Information/Data on NZ Rental Market - Free

The Menu above provides free data galore, it’s worth keeping an Eye on

I realise that many may not notice my homepage Menu above, it’s worth checking, many subscribers do. It includes valuable updates, inventory weekly and rents monthly. I don’t often post about this almost raw data but it is usually self explanatory, especially if you look at any previous post on similar data.

Reminder, every Datawrapper chart I publish will get updated simply by me updating the data which I usually do. This updates ALL previous uses of that chart. Updated charts with out-of-date comments can be a little confusing when looking at an old post where the chart is current. Check the post date compared to the most recent data on the chart when reading my comments which I do not update.

The homepage menu covers four main topics:

Rental Inventory, ie Trademe total listings each Monday

Rental Prices, MBIE pricing detail presented by region in easily understood charts

Sales Inventory, the same as Rental Inventory but for sales in Wellington, Auckland soon

Sales Prices, detail from QV presented in new ways to show direction.

Rental Inventory

I collect inventory stats every Monday morning and it is usually updated here soon after, but I don’t have a schedule. This data is a simple count of the number of properties available for rent on Trademe in each Region (say Auckland or Wellington etc) or District (say Lower Hutt or Porirua etc). This data provides an insight into available supply on each Monday back to 2017. It includes ALL listings, ie those actually advertised at that time, it is not a count of new listings in the month as Trademe or Realestate often publish.

Comparing a specific Monday with the same date the previous year provides a simple and reliable measure that automatically shows seasonal changes in supply.

The sample of Wellington is below to show you how to interpret. Each line shows the measurement on a specific Monday (hover to see the date) and the line is marked to show which year. So mid 2024 is very high compared to any previous year, in fact over double the same time in any year prior to 2022.

Two growth stories seem to apply here,

Supply or Demand changed in 2022 and has not recovered. Supply increased OR demand decreased. Other charts in this menu suggest a big increase in CBD supply, maybe too many apartments being built. All this data and more for Wellington, is on the page above.

Early 2024 a sudden and extreme supply change occurred, apparently sellers deciding to offer their properties for rent after failing to find a buyer. Especially people moving overseas according to Property Managers. I wonder how long this will take to work through the market?

Rental Prices

I collect rental prices from Rental Bond data published by the Tenancy Tribunal (MBIE) every month. I once complained that their data was incorrectly being allocated, their response was to delay the data a month - sorry, the extra month was useful. The issue is that landlords often fail to correctly allocate suburbs and this is corrected later by MBIE. Unfortunately little errors like this is normal when collecting real data so their corrections are a valuable contribution. If they had just told me the problem rather than ceasing publishing I could have allowed for it.

I also collect suburban data for a small number of interesting suburbs in Auckland and Wellington CBDs from here to help understand the CBDs.

Like the Inventory charts, each line represents a year, so for example every June is one above the other. Seasonality is not so strong with rents in most regions. However, for university cities like Wellington, student flats are more expensive at each end of the year. This is because students rent larger 4-6 bedroom flats with higher total rents, and the geographic mean rent method used by MBIE is intended to capture total property rent rather than rent per room.

Wellington example chart below is interesting because you can see the impact of price reductions from January 2023 to April 2023 (thin black line) vs the same times the following year (thin blue line) when supply got very much ahead of demand, this change started in November 2022, suggesting student accomodation was a major cause. New apartments at this time, and maybe still, focussed on the student market, concrete internal walls were introduced, maybe this changed the balance.

Sales Inventory

Sales inventory is almost identical to rental inventory in presentation and data collection methods, ie a count from Trademe every Monday. However seasonality is quite different.

My data currently only applies to Wellington. I have similar data for recent Auckland inventory and will publish as soon as it is useful.

The Wellington Sales inventory shows supply in 2024 (number of homes up for sale) equal to the same time in 2022, ie the middle of the bubble. During the slump in prices in 2023, the number of properties fell to almost the same level as pre-pandemic years 2017/18.

Sales Prices

A new section I am still developing. I collect data from the QV sales price index and present it to show changes in multiple ways. Feedback on methods and charts is very welcome as I try to find useful charts from the data.

The chart below I find interesting, but is one of many charts on this page to explore the relationship between price and other factors I think may be useful to understand the market. I found Household income the most interesting, I did not expect any relationship but early indications are that for similar specifications there is a close relationship. However changes to construction rules change specifications - some a lot, eg 100x50 pine timber treatment.

Market conditions such as interest rates, FOMO (fear of missing out) and FOOP (fear of overpaying) clearly impact this chart. Will the market return to trend once fear retreats?

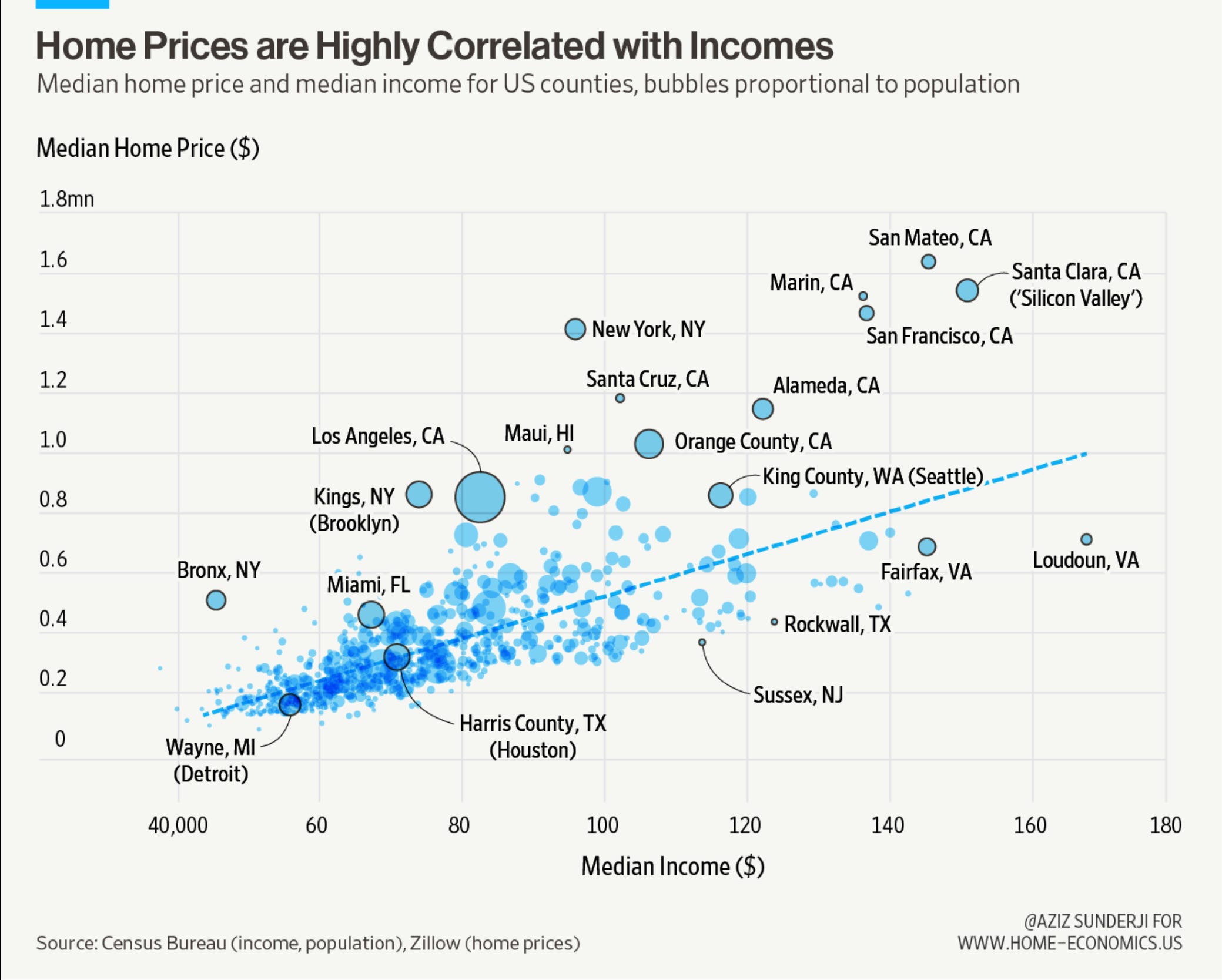

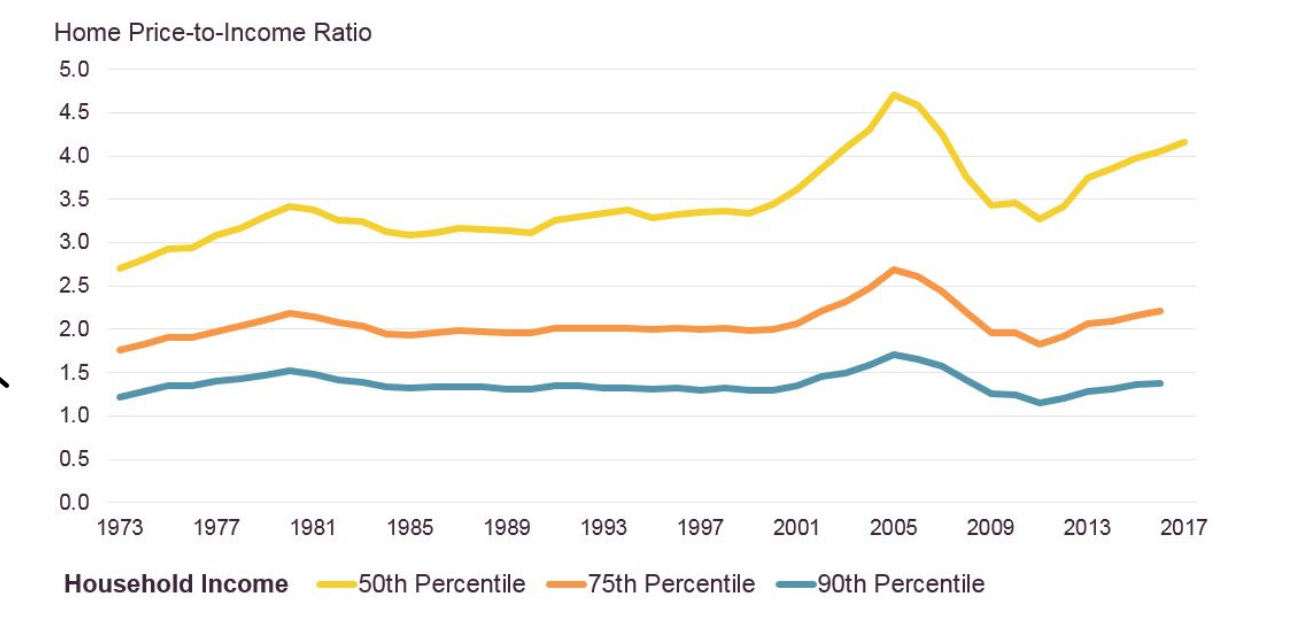

I was so surprised to find prices for homes, like Rents, followed Household Incomes, so have explored that factor. Harvard agree despite the headline here, check out figure 2:

The 50th percentile is also the median, it has been extremely consistent since 1973. Recent increases are a local issue due to increases in interest rates. Home construction costs on flat land with very large numbers of identical homes compared to NZ, lowers the price of new homes in many states, reducing the ratio of Price/Income.

Another substack post from the States that has found similar correlation.